If you’ve ever reached the end of the month wondering where all your money went, you’re in good company. The envelope budgeting method — also known as the cash envelope system — is one of the most effective personal finance strategies ever created. It’s tactile, visual, and surprisingly hard to cheat.

But like any budgeting approach, it comes with real advantages and honest limitations. In this guide, we’ll walk through exactly how the envelope system works, what makes it powerful, where it falls short, and whether it’s the right fit for your financial situation and lifestyle.

| 💡 Quick Summary The envelope budgeting method is a cash-based system where you divide your monthly income into labeled envelopes — one for each spending category. When an envelope is empty, spending in that category stops for the month. It enforces real-time spending limits and eliminates the mystery of where your money disappears each month. |

What Is the Envelope Budgeting Method?

The envelope budgeting method (also called cash stuffing, envelope stuffing, or the cash envelope system) is a zero-based budgeting approach where you assign every dollar of your income to a specific category before the month begins.

Each category gets its own physical envelope — labeled and stuffed with the exact cash amount you’ve budgeted for it. Common envelope categories include:

- Groceries — weekly food shopping

- Rent / Mortgage — fixed housing costs

- Utilities — electricity, internet, gas

- Dining Out — restaurants, coffee, takeout

- Entertainment — movies, hobbies, subscriptions

- Transportation — fuel, transit, parking

- Clothing — personal shopping

- Health & Medical — prescriptions, co-pays

- Savings — emergency fund, sinking fund

- Debt Payoff — extra payments toward loans or cards

The system was popularized by personal finance expert Dave Ramsey and is closely aligned with zero-based budgeting — a philosophy where income minus all assigned expenses equals zero. Every dollar has a job.

The golden rule: when an envelope runs out, spending in that category stops. No borrowing from other envelopes. No swiping a backup card.

How the Cash Envelope System Works — Step by Step

- Calculate your monthly take-home income. Use actual post-tax income, not your gross salary.

- List your budget categories. Think through every regular expense — fixed bills, variable spending, and savings goals.

- Assign a dollar amount to each category. Make sure the total adds up to your income (zero-based approach: every dollar gets allocated).

- Withdraw cash and stuff the envelopes. On payday, visit an ATM or bank, withdraw the total, and sort it into the labeled envelopes.

- Spend only from the correct envelope. Groceries come from the grocery envelope. Gas from transportation. No mixing.

- Stop when the envelope is empty. This is the core discipline that makes the entire system work.

- Review and reset at month’s end. Adjust envelope amounts based on what you learned, and start fresh.

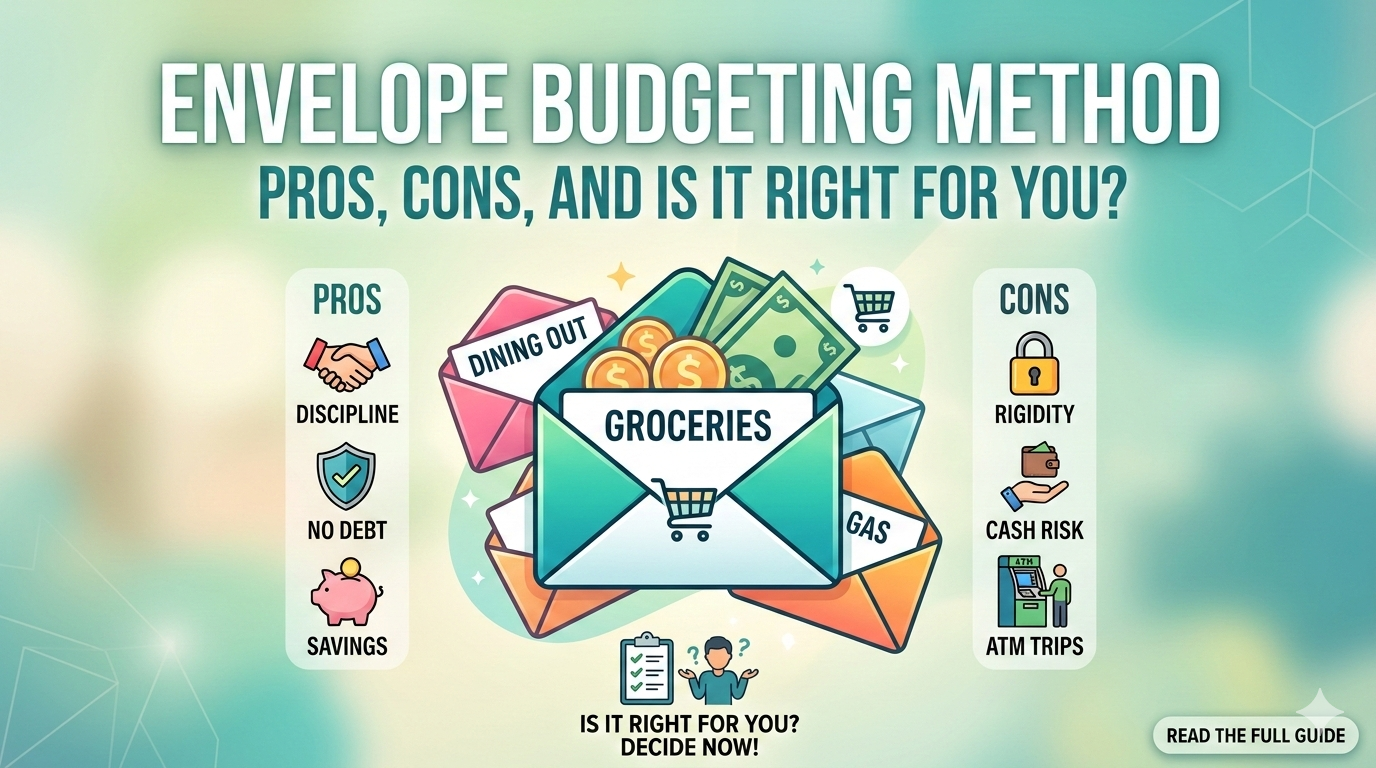

Envelope Budgeting Method: Pros and Cons at a Glance

| ✅ PROS | ❌ CONS |

| ✅ Stops overspending in real time | ❌ Inconvenient to carry cash daily |

| ✅ Zero guesswork — money is pre-assigned | ❌ Not safe — risk of loss or theft |

| ✅ Builds strong cash flow awareness | ❌ Struggles with online payments |

| ✅ Works great for impulse spenders | ❌ Takes time to set up and maintain |

| ✅ No app or internet required | ❌ Hard to split envelopes mid-month |

| ✅ Ideal for irregular income earners | ❌ Not ideal for large purchases |

| ✅ Naturally reduces debt over time | ❌ Requires discipline not to ‘borrow’ |

| ✅ Visual and satisfying to track | ❌ No interest earned on cash |

The Pros of the Envelope Budgeting Method — In Depth

1. It Makes Overspending Physically Impossible

This is the single biggest advantage of the cash envelope system. When the money in your grocery envelope is gone, there’s nothing left to spend. No ‘I’ll pay it back later’ thinking — because there’s nothing to borrow. This is especially powerful for impulse spenders and emotional shoppers.

Behavioral economics research consistently shows that people spend more freely with cards than with cash — a phenomenon known as the ‘pain of paying.’ Physical money makes every purchase more deliberate and more real.

2. Zero Guesswork About Where Your Money Goes

With traditional budgeting, it’s easy to assume you’re on track until you check your bank statement at month’s end. The envelope method eliminates that uncertainty. Every category is funded upfront — you can see at a glance how much is left in any envelope, at any time.

3. Works Without Apps or Technology

Not everyone wants to link their bank accounts to a budgeting app. The cash stuffing method needs nothing more than envelopes, a pen, and your money. It’s one of the most accessible personal finance tools available — ideal for people who are new to budgeting or uncomfortable with digital financial tracking.

4. Perfect for Variable and Irregular Income

Freelancers, gig workers, and seasonal earners often struggle with cash flow management because their monthly income shifts. The envelope system adapts naturally — you budget based on actual money received this month, not an estimate. Earn $3,200? Stuff $3,200. Earn $2,600? Adjust accordingly.

5. Naturally Reduces Debt Over Time

When you can only spend what’s in an envelope, you stop supplementing shortfalls with credit cards. Many people using the envelope system as part of a debt payoff plan — especially Dave Ramsey’s Baby Steps — report accelerating their debt freedom because overspending simply isn’t an option anymore.

6. Builds Genuine Financial Awareness

Most people dramatically underestimate how much they spend on dining out, entertainment, and personal care. Physically handling cash for each category creates a level of financial awareness that digital tools rarely match. Many envelope budgeters describe their first month as a genuine ‘wake-up call.’

7. Excellent for Teaching Kids About Money

The cash envelope system for families is one of the best tools for introducing children to money management. Kids can visually understand that when the ‘fun money’ envelope is empty, fun stops until next month — building habits of delayed gratification and financial responsibility early in life.

The Cons of the Envelope Budgeting Method — Honestly Assessed

1. Carrying Cash Is Inconvenient and Risky

The most practical downside of physical envelope budgeting is that it requires carrying cash — sometimes significant amounts. If your wallet is lost or stolen, that money is gone. Unlike a debit card, there’s no fraud protection, no dispute resolution, and no recovery. This is a real safety concern, particularly in urban areas or while traveling.

2. Online Shopping and Auto-Payments Are a Problem

We live in a digital economy. Amazon orders, subscription services, automatic bill payments — none of these work with physical cash. This is one of the biggest practical cons of the envelope budgeting method today. You’ll need workarounds (using a debit card and manually deducting from your envelope balance) that add friction to an otherwise simple system.

3. Time-Consuming Setup and Maintenance

Visiting the ATM, withdrawing exact amounts, and sorting bills into envelopes takes time — every payday. For busy professionals or parents managing tight schedules, this friction can make the system feel unsustainable compared to budgeting apps like YNAB or Mint that sync and categorize transactions automatically.

4. Managing Multiple Categories Gets Complicated

If your monthly budget has 15 to 20 categories, managing that many envelopes becomes genuinely cumbersome. Mid-month surprises — like an unexpected car repair — require physically redistributing cash between envelopes and recalculating everything. More categories mean more organizational overhead.

5. You Forfeit Rewards and Interest

Cash earns nothing. If you typically use a rewards credit card and pay it off monthly, switching to cash means giving up cashback, travel points, or miles. And cash sitting in envelopes earns zero interest, whereas even a basic high-yield savings account lets your money grow between payday and spending day.

6. Requires Discipline Not to Borrow Between Envelopes

The system only works if you respect its core rule. But when the dining envelope runs dry mid-month and friends invite you out, the temptation to pull from entertainment or personal care is real. This ‘envelope borrowing’ gradually unravels the system and is one of the most common reasons people quit within the first few months.

The Digital Envelope Budgeting Alternative

The digital envelope system solves most of the cash-related drawbacks while preserving the core logic of the original. Instead of physical cash, you use virtual envelopes — sub-accounts or spending categories inside an app — to pre-allocate your income before it’s spent.

Popular tools that replicate the envelope method digitally:

- YNAB (You Need A Budget) — the gold standard for digital zero-based budgeting

- Goodbudget — a dedicated virtual envelope app with a solid free tier

- EveryDollar — Dave Ramsey’s official zero-based budgeting app

- Qube Money — a debit card with built-in virtual envelope control

- Google Sheets / Excel templates — custom-built digital envelope trackers

Digital envelope budgeting preserves the zero-based discipline while accommodating the reality of card payments, online shopping, and recurring subscriptions. For most modern budgeters, it’s the best of both worlds.

| 🔄 Hybrid Approach Tip Many successful budgeters use a hybrid system: physical cash envelopes for high-temptation variable categories (groceries, dining, entertainment) and a digital tracker for fixed bills and online expenses. You get the psychological power of cash where it matters most — without the inconvenience for predictable monthly payments. |

Who Should Use the Envelope Budgeting Method?

The Cash Envelope System Works Best For:

- Budgeting beginners who need a simple, visual system to start

- Chronic overspenders who find it easy to swipe cards but feel the impact with cash

- Families who want to teach children healthy money habits

- People on a debt payoff journey who need firm spending limits

- Variable income earners such as freelancers, contractors, and gig workers

- Anyone who prefers offline, technology-free personal finance

The Envelope Method May Not Suit:

- Frequent online shoppers who make most purchases digitally

- Business owners with complex multi-category expense needs

- Heavy credit card rewards users who pay off balances in full monthly

- People unwilling to make regular ATM trips or manage physical cash

Frequently Asked Questions

Is the envelope budgeting method effective?

Yes. Research in behavioral finance — and decades of real-world results — consistently show that cash-based budgeting reduces discretionary overspending. The physical act of handling cash makes spending feel more deliberate. Effectiveness depends on consistency, but most people who stick with the system for 90 days report meaningful changes in their spending habits.

How many envelopes should I start with?

Beginners should start with 5 to 8 envelopes — the categories where you most commonly overspend. Groceries, dining out, entertainment, transportation, and personal care are great starting points. Add more categories gradually once the habit is established.

What do I do with leftover cash at month’s end?

Three solid options: roll it over into the same envelope next month (useful for irregular expenses like clothing or car maintenance), move it to your emergency fund or sinking fund, or apply it as an extra payment toward debt. Most personal finance coaches recommend building your emergency fund first.

Can I use the envelope method with a debit card?

Absolutely — this is the digital envelope system. Apps like YNAB and Goodbudget let you track virtual envelopes while paying with a card. The discipline of manually (or automatically) recording each transaction against its envelope is what keeps the system honest.

Is envelope budgeting the same as zero-based budgeting?

They share the same philosophy — every dollar gets a purpose before it’s spent — but aren’t identical. Zero-based budgeting is a broader strategy. Envelope budgeting is one specific implementation of it. You can do zero-based budgeting with a spreadsheet or app without ever using an envelope.

Final Verdict: Is the Envelope Budgeting Method Worth It?

Yes — if you’re ready to take real control of your spending. The envelope budgeting method has helped millions of people stop living paycheck to paycheck, get out of debt, and build their first emergency fund. Its power isn’t magic — it’s psychology. Cash feels real in a way that a card swipe doesn’t.

For anyone who finds traditional budgeting apps abstract or easy to ignore, the cash envelope system offers something those tools can’t: a physical boundary that you can see, touch, and respect.

If all-cash living feels impractical, try a digital envelope app or a hybrid approach. The format matters less than the principle: decide where your money goes before you spend it — then honor that decision.

| 🚀 Start Simple Begin with just 3 envelopes: Groceries, Dining Out, and Entertainment. These are the three categories most people overspend on. Track them with cash for one month. The difference in your awareness — and your bank balance — will likely convince you to keep going. |

Conclusion

The envelope budgeting method is a time-tested personal finance strategy with clear, honest pros and cons. Its greatest strength is psychological: cash changes behavior in ways that digital tools often can’t. Its greatest limitation is practicality: a cashless economy creates genuine friction for all-physical systems.

Whether you choose physical envelopes, a digital envelope app, or a hybrid approach, the core discipline remains the same: assign every dollar a purpose before you spend it. Start with a few categories, build the habit, and watch your financial picture change.