If you’ve ever reached the end of the month and wondered where all your money went, you’re not alone. The envelope budgeting method is one of the oldest and most effective personal finance strategies out there — and it’s making a major comeback.

Whether you’re just starting your financial journey or looking to take better control of your spending habits, understanding the pros and cons of the envelope system can help you decide if it’s the right budgeting technique for you.

In this guide, we’ll break down exactly how the envelope budget system works, explore its real-world benefits and drawbacks, and share tips to make it work in today’s digital world.

What Is the Envelope Budgeting Method?

The envelope budgeting method — sometimes called the cash envelope system or cash stuffing — is a zero-based budgeting strategy where you divide your monthly income into physical (or digital) envelopes, each labeled for a specific spending category. Once an envelope is empty, you stop spending in that category until the next budget period begins.

For example, you might create envelopes for:

- Groceries — $400

- Dining out — $150

- Transportation — $200

- Entertainment — $100

- Utilities — $180

Popularized by personal finance expert Dave Ramsey, the envelope system is rooted in behavioural economics: when you physically handle cash and watch it disappear, you become far more mindful of your spending decisions. That tangible connection to money is what makes this budgeting method uniquely powerful compared to simply tracking expenses in a spreadsheet or an app.

How the Envelope Budget System Works: Step by Step

Setting up an envelope budgeting system is straightforward. Here’s how to get started:

- Calculate your monthly take-home income. Start with the actual amount deposited into your bank account each month after taxes.

- List your spending categories. Think about every area where you spend money: housing, food, transport, personal care, savings, and discretionary spending.

- Assign a dollar amount to each category. Every dollar of your income should be assigned to an envelope. This is the zero-based budgeting principle — income minus expenses equals zero.

- Withdraw cash and stuff your envelopes. At the start of each pay period, withdraw the allocated cash and physically place it in each labeled envelope.

- Spend only from the envelope. When you shop, use only the cash from the designated envelope. When it’s gone, it’s gone.

- Review and adjust. At month’s end, review your envelopes, roll over any leftover cash or apply it to debt, and adjust allocations as needed.

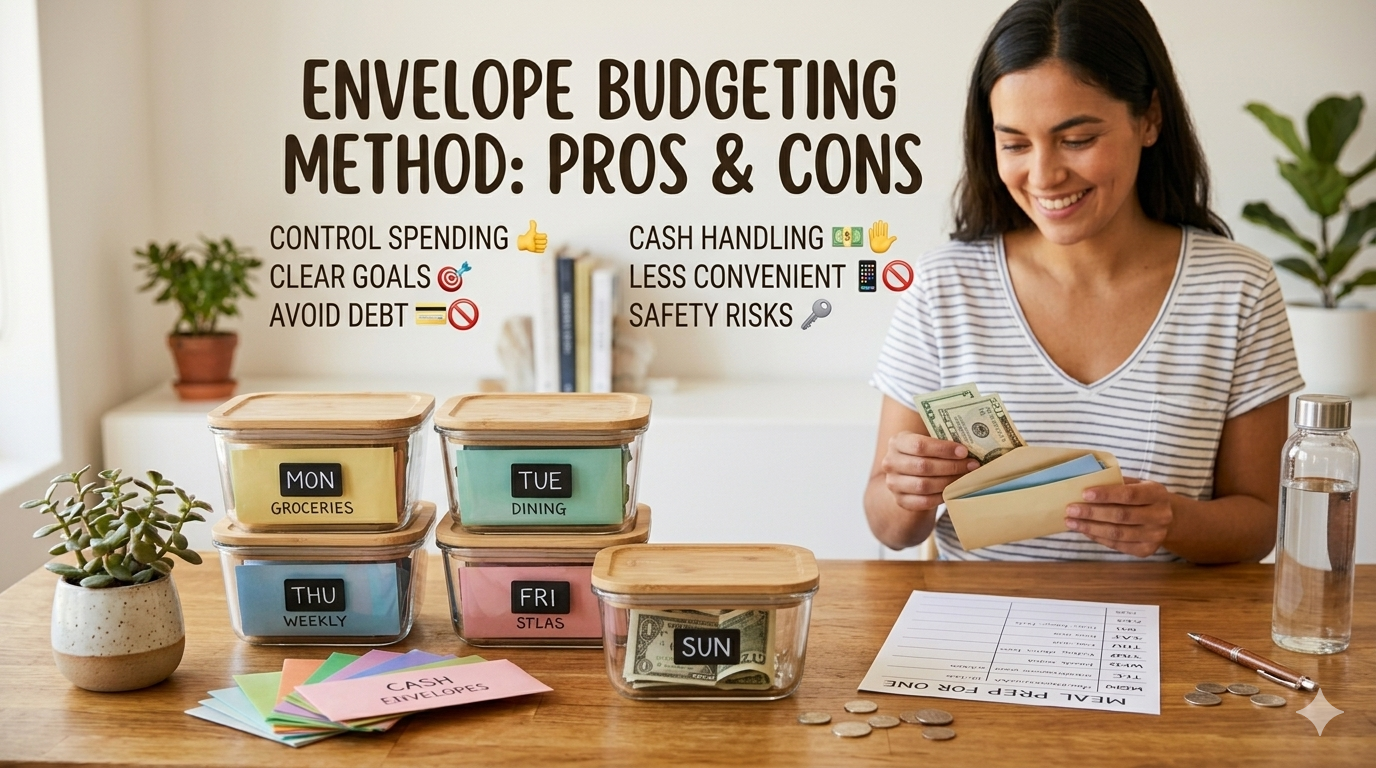

Envelope Budgeting Method: The Pros

Let’s dive into the most compelling benefits of the envelope system and why millions of people swear by this cash management strategy.

1. Creates Powerful Spending Awareness

One of the biggest advantages of cash envelope budgeting is how it changes your psychological relationship with money. Research in consumer behaviour consistently shows that people spend significantly more when paying with cards compared to cash. When you physically hand over bills, your brain registers the loss more acutely — reducing impulse purchases and encouraging thoughtful spending. This is often called the ‘pain of paying.’

2. Prevents Overspending in Every Category

Unlike digital spending where it’s easy to overspend without noticing until the end of the month, the envelope method creates a hard limit. You simply cannot spend more than what’s in the envelope. This built-in spending cap is particularly helpful for people struggling with discretionary spending categories like dining out, clothing, or entertainment.

3. Works for All Income Levels

Whether you earn $2,000 a month or $10,000, the envelope budget system scales to your income. It’s especially powerful for people on a tight budget, irregular income earners like freelancers, and anyone recovering from debt. The system doesn’t require a minimum income — it simply requires commitment and consistency.

4. Accelerates Debt Payoff and Savings Goals

Many financial coaches and debt-free communities credit the envelope method as a critical tool in paying off debt quickly. By capping discretionary spending and making every dollar intentional, you can free up more money for debt repayment or building an emergency fund. Dave Ramsey’s Baby Steps program, which uses this system, has helped thousands of families eliminate debt and reach financial freedom.

5. Simple and Requires No Technology

The envelope budgeting system has zero learning curve. There’s no app to download, no software to configure, and no subscription fee. All you need is a few envelopes, a pen, and your cash. This simplicity makes it accessible to people of all ages and tech comfort levels — including seniors, teenagers learning money management, and individuals without smartphones.

6. Builds Healthy Financial Habits

Budgeting with envelopes is a habit-building exercise. Over time, the discipline of allocating money to categories before spending teaches financial planning skills that translate to every area of your financial life — from investing to saving for big purchases. It’s particularly effective for people who struggle with impulse buying or have never followed a budget before.

Envelope Budgeting Method: The Cons

Like any budgeting approach, the envelope system has real limitations. Here’s an honest look at the disadvantages you should consider before committing.

1. Carrying Cash Is Inconvenient and Risky

One of the most cited drawbacks of the cash envelope method is the sheer inconvenience of carrying physical cash. Withdrawing money, organising it into envelopes, and then remembering to bring the right envelope when you go shopping adds friction to everyday life. More importantly, cash that’s lost or stolen is gone — unlike a credit or debit card, there’s no fraud protection or recovery option.

2. Doesn’t Work Well for Online Shopping

We live in an increasingly cashless society. A huge portion of modern spending happens online — from Amazon purchases to streaming subscriptions to bill payments. The traditional cash envelope system doesn’t naturally accommodate these digital transactions, requiring workarounds like withdrawing cash and then depositing it back, or using a separate tracking method for online spending.

3. Misses Out on Rewards and Cashback

If you’re a disciplined spender, using a rewards credit card for everyday purchases can earn significant cashback, travel miles, or points. The envelope method requires you to use cash, which means you forfeit these benefits. For people who pay their full balance each month and never carry debt, this is a notable financial opportunity cost.

4. Requires Frequent Bank Visits

Maintaining a cash-based budgeting system means regular trips to the ATM or bank to withdraw specific amounts. This isn’t just time-consuming — ATM fees can also eat into your budget, especially if you bank with an institution that charges for withdrawals or doesn’t have convenient locations.

5. Can Be Rigid in Emergency Situations

What happens when you run out of grocery money mid-month? The strict rules of the envelope system can feel inflexible when unexpected expenses arise — a car breakdown, a medical bill, or a social occasion you hadn’t planned for. Without an emergency fund envelope or a clear process for handling these situations, the system can cause stress rather than relieve it.

6. Not Ideal for Couples Without Communication

For couples managing shared finances, the envelope system requires consistent communication and agreement on spending rules. If one partner withdraws cash and spends from an envelope without telling the other, the system breaks down. Without alignment on financial goals and mutual accountability, the envelope method can create conflict rather than cooperation.

The Digital Envelope System: A Modern Alternative

If the idea of carrying cash makes you nervous, or you do most of your spending online, you’ll be glad to know there’s a modern solution: the digital envelope budgeting system. Apps like YNAB (You Need A Budget), Goodbudget, and Mvelopes bring the same envelope-based philosophy to your smartphone.

With these virtual envelope budgeting apps, you:

- Create virtual envelopes for each spending category

- Assign your income digitally across categories

- Log transactions manually or sync with your bank

- View real-time balances to stay on track

This approach preserves all the core advantages of envelope budgeting — intentional spending, category limits, and financial awareness — while eliminating the practical downsides of physical cash. It’s also ideal for tracking irregular expenses, annual bills, and sinking funds like holiday gifts or car maintenance.

Who Should Use the Envelope Budgeting Method?

The envelope system isn’t one-size-fits-all, but it’s particularly well-suited for:

- People paying off debt who need strict control over discretionary spending

- First-time budgeters who want a simple, tactile system to start with

- Impulse spenders who need a physical barrier between them and their money

- Families on a fixed income trying to make every dollar count

- Anyone who struggles to save or feels their money disappears without explanation

It may be less ideal for high earners with complex finances, frequent online shoppers, or those who already have strong budgeting habits and prefer digital tools.

Tips to Make the Envelope Method Work for You

- Start with just a few envelopes. Don’t try to categorize every single expense right away. Begin with 4–5 problem areas where you tend to overspend.

- Include a ‘misc’ or ‘buffer’ envelope. Set aside a small amount for unexpected expenses so you’re not derailed by small surprises.

- Build a sinking fund envelope. Save a small amount monthly for predictable irregular expenses like annual insurance premiums, holiday gifts, or back-to-school shopping.

- Label envelopes clearly. Write the category, the allocated amount, and the budget period on each envelope to avoid confusion.

- Hold weekly check-ins. Take 10 minutes each week to review your envelope balances and adjust your spending plan if needed.

Envelope Budgeting vs. Other Popular Budgeting Methods

Wondering how the envelope method stacks up against other budgeting strategies? Here’s a quick comparison:

Envelope Method vs. 50/30/20 Rule: The 50/30/20 rule divides income into needs (50%), wants (30%), and savings (20%). It’s less granular than the envelope method and doesn’t require cash, making it simpler but less controlling for problem spenders.

Envelope Method vs. Zero-Based Budgeting: The envelope method is essentially a hands-on version of zero-based budgeting. Both assign every dollar a purpose, but zero-based budgeting is often done digitally with software like YNAB or a spreadsheet.

Envelope Method vs. Pay Yourself First: Pay yourself first prioritises savings before anything else. It’s a great complement to envelope budgeting — you can simply make savings its own envelope and fund it before distributing the rest.

Frequently Asked Questions About Envelope Budgeting

Is the envelope budgeting method effective?

Yes — for the right person. Studies and anecdotal evidence both support the idea that tangible cash budgeting reduces overspending. It’s especially effective for those with impulse spending problems or anyone new to budgeting.

Can I do envelope budgeting without cash?

Absolutely. Digital envelope budgeting apps like YNAB, Goodbudget, and EveryDollar replicate the envelope system virtually, making it compatible with online spending, debit cards, and direct deposits.

How many envelopes should I have?

Most financial experts recommend between 5 and 10 envelopes. Too few and you lack granularity; too many and the system becomes overwhelming. Start small and add categories as you get comfortable.

What do I do if I run out of money in an envelope?

Stop spending in that category, or consciously borrow from another envelope. The key is to make it a deliberate decision, not an automatic one. If it happens repeatedly, adjust your budget allocation for that category.

Final Verdict: Is the Envelope Budgeting Method Right for You?

The envelope budgeting method is a time-tested, psychologically powerful approach to personal finance that genuinely works for millions of people. Its core strength lies in creating tangible spending awareness and hard category limits that digital budgeting methods often fail to enforce.

That said, it’s not perfect. The inconvenience of cash, incompatibility with online purchases, and missed rewards are real drawbacks — but all are solvable with digital alternatives and a bit of planning.

If you’re struggling with overspending, trying to pay off debt, or simply want to feel more in control of your money, give the envelope system a try for 30 days. You might be surprised by just how transformative it can be to see exactly where every dollar goes.